Credit And Collections Software: The Complete 2026 Guide To AI-Powered Debt Recovery Solutions

Introduction

The collections industry is undergoing a fundamental transformation. As debt portfolios grow more complex and regulatory requirements tighten, traditional collection methods are no longer sufficient. Credit and collections software has evolved from simple account tracking systems into sophisticated AI-powered platforms that automate outreach, ensure compliance, and dramatically improve recovery rates. For Collections Managers, Directors of Operations, and CFOs overseeing accounts receivable departments, choosing the right credit and collections software is now a strategic imperative rather than a tactical decision.

This comprehensive guide explores how modern credit and collections software leverages artificial intelligence, what features matter most for maximizing recovery while maintaining compliance, and how to evaluate platforms that can scale with your agency's growth. Whether you manage a dedicated collection agency or an enterprise AR department, understanding the current landscape of credit and collections software will help you make informed decisions that directly impact your bottom line.

Understanding Credit and Collections Software in 2026

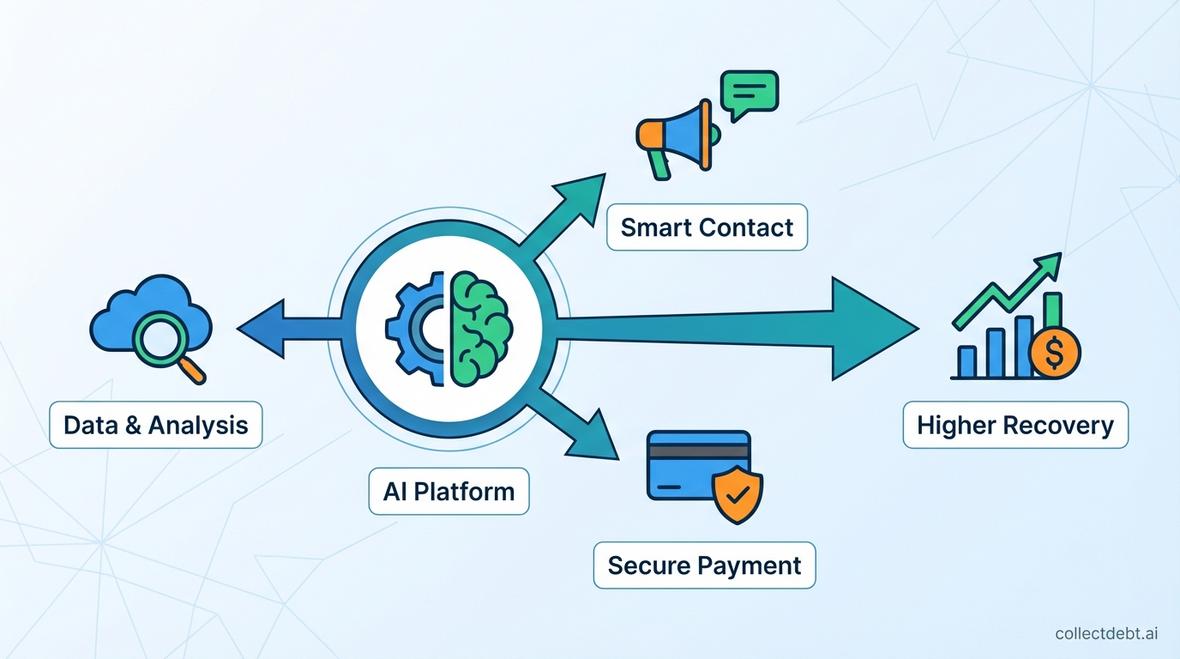

Credit and collections software encompasses digital platforms designed to manage the entire debt recovery lifecycle from initial account placement through final resolution. Modern solutions integrate multiple functions: account management, communication workflows, payment processing, compliance monitoring, and analytics. The most advanced platforms now incorporate artificial intelligence to automate contact strategies, personalize debtor interactions, and predict which accounts are most likely to pay.

The evolution of credit and collections software reflects broader technological trends. Early systems focused primarily on data organization and manual workflow support. Today's platforms function as autonomous agents capable of conducting full collection conversations across voice, SMS, email, and chat channels. AI/ML Integration Key Trend Driving Debt Collection Software Adoption shows how advanced technologies like AI and ML are now central to credit risk assessment, workflow automation, and real-time credit bureau integration to optimize strategies and compliance.

Key Components of Modern Credit and Collections Software

Effective credit and collections software typically includes several core components:

- Account Management System: Centralized database tracking debtor information, payment history, communication logs, and account status

- Omnichannel Communication Engine: Integrated platforms for voice, SMS, email, and chat outreach with intelligent channel selection

- Payment Processing: Secure digital payment acceptance with multiple options including ACH, credit cards, and payment plans

- Compliance Framework: Built-in rule engines ensuring adherence to FDCPA, TCPA, CFPB regulations, and state-specific requirements

- Analytics and Reporting: Real-time dashboards tracking key performance indicators like contact rates, promise-to-pay conversion, and liquidation rates

- Integration Capabilities: APIs connecting to CRMs, credit bureaus, accounting systems, and other enterprise software

The end-to-end collection solutions available today represent a significant advancement over legacy systems, offering seamless workflows from first contact through final payment.

The AI Transformation of Credit and Collections Software

Artificial intelligence represents the most significant advancement in credit and collections software over the past five years. AI-powered platforms can now conduct natural conversations with debtors, understand intent, negotiate payment arrangements, and escalate complex cases to human agents all while maintaining perfect compliance with regulatory requirements.

Conversational AI Capabilities

Modern AI agents in collections software utilize natural language processing to understand debtor responses, context, and sentiment. These systems can handle objections, answer questions about account details, explain payment options, and even detect financial hardship indicators that may warrant alternative resolution strategies. Conversational AI in debt collection has matured to the point where many debtors cannot distinguish between AI and human agents during routine interactions.

The capabilities include:

- Intent Recognition: Understanding whether a debtor is disputing the debt, requesting validation, expressing willingness to pay, or seeking hardship assistance

- Dynamic Script Adaptation: Adjusting conversation flow based on debtor responses rather than following rigid scripts

- Sentiment Analysis: Detecting frustration, confusion, or distress and modifying tone and approach accordingly

- Multilingual Support: Conducting collections conversations in multiple languages without requiring dedicated multilingual staff

Predictive Analytics and Account Prioritization

AI-driven credit and collections software leverages machine learning models trained on historical recovery data to predict which accounts are most likely to pay and which contact strategies will be most effective. This capability allows agencies to allocate resources efficiently, focusing human collector time on high-value, complex accounts while automating routine collections through AI agents.

Predictive models analyze factors including payment history, demographic information, account age, debt amount, previous contact outcomes, and external economic indicators. The software then assigns propensity-to-pay scores and recommends optimal contact strategies including channel preference, time of day, message framing, and settlement offer parameters.

Compliance and Regulatory Considerations in Collections Software

For decision-makers evaluating credit and collections software, compliance capabilities are non-negotiable. Regulatory violations can result in substantial fines, legal action, and reputational damage that far exceeds any operational savings from inadequate software. Modern platforms must provide comprehensive compliance frameworks that adapt to evolving regulations.

FDCPA and TCPA Compliance

The Fair Debt Collection Practices Act and Telephone Consumer Protection Act establish strict requirements for collection communications. Effective credit and collections software automates compliance through features such as:

- Call Time Restrictions: Automatically blocking outbound calls outside permitted hours based on debtor time zones

- Communication Frequency Limits: Tracking contact attempts across all channels to prevent excessive contact

- Consent Management: Maintaining records of communication preferences and consent for calls/texts to mobile numbers

- Cease and Desist Tracking: Immediately flagging accounts where debtors have requested no further contact

- Mini-Miranda Disclosure: Ensuring all communications include required debt collector identification

The compliance solutions embedded in advanced platforms provide audit trails documenting that every interaction meets regulatory standards, which is essential for defending against consumer complaints.

Adaptive Regulatory Frameworks

Regulations governing debt collection vary significantly across states and continue to evolve. Leading credit and collections software platforms incorporate rule engines that automatically apply jurisdiction-specific requirements based on debtor location. When regulations change, these systems can be updated centrally, ensuring immediate compliance across all operations without requiring manual process changes.

Essential Features to Evaluate in Credit and Collections Software

When selecting credit and collections software, decision-makers should assess platforms across several critical dimensions that directly impact operational efficiency and recovery outcomes.

Omnichannel Communication Capabilities

Debtors have distinct communication preferences. Some respond best to phone calls, others to text messages, and still others prefer email or self-service portals. Comprehensive credit and collections software supports coordinated outreach across all channels while maintaining conversation context regardless of where interactions occur.

The omnichannel support provided by modern platforms ensures that if a debtor begins a conversation via SMS but later calls in, the AI agent has full context of previous interactions and can continue the conversation seamlessly. Customer-Centric Collections Software Reduces Disputes and Improves Cash Flow by emphasizing customer experience through integrations, AI analytics, and multichannel tools that reduce disputes and enhance engagement.

Self-Service Payment Options

Many debtors prefer to resolve obligations without speaking to a collector. Credit and collections software that includes robust self-service capabilities including payment portals, automated payment plan setup, and account information access significantly improves recovery rates while reducing operational costs.

Digital Payments and Self-Service Portals Boost Recovery in Debt Collection through online payments, automated reminders, and personalized payment plans that enhance debtor satisfaction and operational efficiency. The self-service debt resolution features available today allow debtors to manage their accounts 24/7, leading to faster resolutions and improved debtor satisfaction.

Integration Ecosystem

No collection software operates in isolation. Effective platforms must integrate seamlessly with existing systems including CRM platforms, accounting software, credit bureaus, and legal management systems. APIs and pre-built connectors reduce implementation time and ensure data consistency across your technology stack.

The integration capabilities of your chosen platform will determine how easily it fits into your existing workflow and whether you can achieve a single source of truth for account data.

Analytics and Reporting

Data-driven decision-making requires comprehensive analytics. The best credit and collections software provides real-time dashboards tracking metrics such as:

- Right Party Contact (RPC) rates

- Promise-to-Pay (PTP) conversion rates

- Liquidation rates by portfolio, collector, and strategy

- Cost per dollar collected

- Compliance metrics and risk indicators

- Channel effectiveness comparisons

Advanced platforms also offer post-call analysis capabilities that use AI to evaluate conversation quality, identify coaching opportunities, and detect compliance risks in recorded interactions.

ROI and Cost Considerations for Collections Software

The investment in credit and collections software must be justified by demonstrable returns in recovery rates, operational efficiency, and risk reduction. Understanding the total cost of ownership and expected ROI is essential for securing stakeholder buy-in.

Direct Cost Components

Pricing models for credit and collections software vary considerably:

- Subscription-based: Monthly or annual fees based on user count, account volume, or communication volume

- Performance-based: Percentage of recovered amounts, aligning vendor success with client outcomes

- Hybrid models: Combining base subscription fees with performance bonuses

Beyond software licensing, consider implementation costs, training expenses, integration development, and ongoing support fees when calculating total investment.

Measuring ROI

Effective credit and collections software delivers ROI through multiple channels:

- Increased Recovery Rates: AI-powered platforms typically improve liquidation rates by 15-30% through optimized contact strategies and personalized communication

- Reduced Operational Costs: Automation reduces the need for large call center teams, with AI agents handling routine collections at a fraction of human labor costs

- Improved Compliance: Automated compliance reduces the risk of regulatory violations and associated fines

- Faster Resolution Times: Omnichannel capabilities and self-service options accelerate payment cycles

- Enhanced Scalability: AI-driven platforms can handle volume increases without proportional cost increases

Organizations implementing advanced AI debt collection automation frequently report payback periods of less than six months due to the combination of increased recoveries and reduced operational expenses.

Industry-Specific Considerations for Collections Software

Different industries face unique challenges in debt collection that influence credit and collections software requirements.

Healthcare Collections

Medical debt collection requires sensitivity to patient relationships and compliance with HIPAA regulations. Credit and collections software for healthcare must support payment plan negotiations, insurance verification, and compassionate communication approaches that preserve patient-provider relationships while recovering outstanding balances.

Financial Services

Financial services collections involve complex products including credit cards, personal loans, and mortgages. Software platforms must handle sophisticated account structures, support skip tracing capabilities, and integrate with credit reporting systems to accurately reflect account status.

Utilities and Telecom

Utilities and telecom companies face high-volume, relatively low-balance collections with specific regulatory requirements around service disconnection notices. Effective credit and collections software for these industries emphasizes automation, self-service payment options, and integration with billing systems.

Auto Finance

The auto finance sector requires collections software that can coordinate payment recovery efforts with repossession management, handle complex state-specific regulations around vehicle seizure, and support redemption processes.

Implementation Best Practices for Collections Software

Successfully deploying new credit and collections software requires careful planning and change management to ensure adoption and realize expected benefits.

Assessment and Requirements Gathering

Begin by documenting current processes, pain points, and specific requirements. Involve stakeholders across operations, compliance, IT, and finance to ensure the selected platform addresses all organizational needs. Define success metrics that will be used to evaluate platform performance post-implementation.

Data Migration Strategy

Migrating account data from legacy systems represents a significant implementation challenge. Develop a comprehensive data migration plan that includes data cleansing, validation protocols, and phased migration approaches to minimize disruption. Ensure historical communication logs and payment data transfer accurately to maintain compliance documentation.

Training and Adoption

Even the most sophisticated credit and collections software delivers value only when staff use it effectively. Invest in comprehensive training programs covering both technical operation and strategic use of platform features. Consider phased rollouts that allow teams to master core functionality before introducing advanced features.

Continuous Optimization

Post-implementation, establish regular review cycles to analyze platform performance, identify optimization opportunities, and adjust strategies based on results. Modern credit and collections software provides extensive analytics that should inform ongoing process refinements.

Future Trends in Collections Technology

The credit and collections software landscape continues to evolve rapidly. Several emerging trends will shape the industry over the next several years.

Advanced AI Capabilities

Next-generation AI agents will demonstrate even greater sophistication in understanding debtor circumstances, detecting financial hardship, and recommending optimal resolution strategies. Emotional intelligence capabilities will enable AI to adjust communication approaches based on debtor stress levels and communication styles.

Blockchain for Verification

Blockchain technology may address long-standing challenges in debt verification and chain of custody documentation, providing immutable records of account ownership and communication history that could reduce disputes and streamline legal processes.

Enhanced Personalization

Machine learning models will enable increasingly granular personalization of collection strategies based not just on demographic and account characteristics but on behavioral patterns, communication preferences, and predicted life events that may affect payment capacity.

Selecting the Right Credit and Collections Software Platform

Choosing credit and collections software represents a significant strategic decision with long-term implications for recovery performance and operational efficiency. Decision-makers should evaluate platforms across several dimensions:

- Technology Foundation: Is the platform built on modern, scalable architecture that can grow with your organization?

- AI Capabilities: Does the solution leverage genuine AI for conversation, prediction, and optimization rather than simple automation?

- Compliance Framework: Are regulatory requirements embedded in the system with automatic updates as regulations evolve?

- Integration Capabilities: Can the platform connect seamlessly with your existing technology ecosystem?

- Vendor Stability: Is the vendor financially stable with a track record of ongoing platform investment and customer support?

- Industry Expertise: Does the vendor understand the specific challenges and requirements of your industry?

Platforms like AI debt collection solutions from CollectDebt.ai represent the current state-of-the-art, combining advanced conversational AI, comprehensive compliance frameworks, and proven results across multiple industries.

Frequently Asked Questions

What is the difference between collections software and accounts receivable software?

While related, these platforms serve different purposes. Accounts receivable software primarily manages invoicing, payment processing, and AR aging for current customers. Collections software focuses specifically on recovering past-due accounts, often after they have been charged off or placed with an agency. Modern platforms increasingly combine both functions into integrated solutions.

How does AI collections software maintain compliance with FDCPA regulations?

AI-powered credit and collections software maintains compliance through embedded rule engines that automatically apply regulatory requirements. These systems track communication frequency, enforce call time restrictions, manage consent for mobile contacts, and ensure all disclosures are provided. Every interaction is logged with detailed audit trails that document compliance with FDCPA, TCPA, and other regulations.

Can collections software integrate with existing CRM and accounting systems?

Yes, modern credit and collections software is designed with integration as a core capability. Most platforms offer APIs and pre-built connectors for popular CRM systems, accounting platforms, and other enterprise software. This ensures seamless data flow and eliminates manual data entry between systems.

What ROI can organizations expect from implementing AI-powered collections software?

ROI varies based on organization size, portfolio characteristics, and previous collection effectiveness. However, organizations typically report 15-30% improvements in recovery rates, 40-60% reductions in operational costs through automation, and payback periods of 3-6 months. The combination of increased recoveries and reduced costs often delivers ROI exceeding 200% in the first year.

How does collections software handle different debtor communication preferences?

Comprehensive credit and collections software supports omnichannel communication, allowing debtors to interact via their preferred channel phone, SMS, email, or web chat. The platform maintains conversation context across channels, so interactions remain coherent regardless of where they occur. AI agents can also predict which channel will be most effective for each debtor based on historical response patterns.

Conclusion

The evolution of credit and collections software from basic account management systems to sophisticated AI-powered platforms has fundamentally transformed debt recovery operations. For Collections Managers, Operations Directors, and CFOs, selecting the right platform is no longer just about digitizing existing processes it is about leveraging technology to achieve recovery outcomes that were impossible with traditional methods.

Modern credit and collections software delivers measurable improvements in recovery rates, operational efficiency, and compliance while simultaneously improving debtor experiences through personalized, respectful communication. As AI capabilities continue to advance and regulatory requirements evolve, organizations that invest in cutting-edge platforms position themselves for sustained competitive advantage in an increasingly challenging collections environment. The decision you make today about credit and collections software will shape your organization's recovery performance for years to come.

Ready to Transform Your Collections Process?

See how CollectDebt.ai can help you automate debt collection, reduce costs, and improve compliance.