Charge Off Vs Collection: Complete 2026 Guide To Debt Recovery Strategies For Decision-Makers

Understanding the Critical Difference: Charge Off vs Collection

For decision-makers in debt collection agencies and accounts receivable departments, understanding the distinction between charge off vs collection is fundamental to maximizing recovery rates while maintaining regulatory compliance. These two concepts represent different stages and strategies in the debt recovery lifecycle, each with distinct financial, operational, and legal implications.

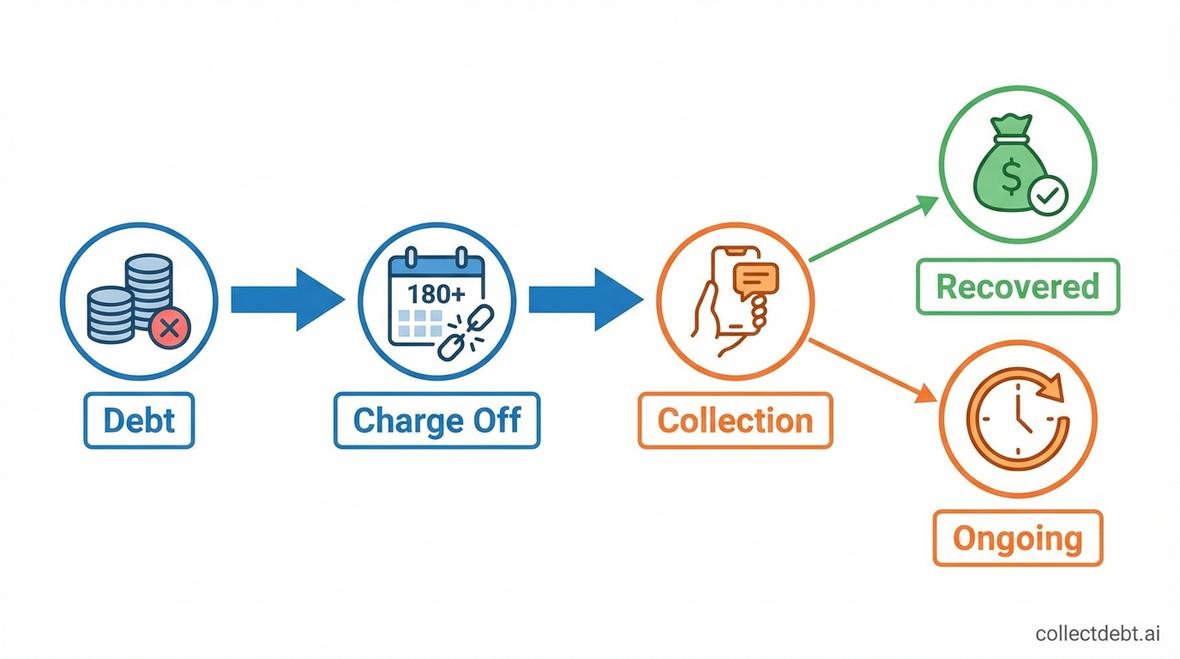

A charge-off occurs when a creditor determines that a debt is unlikely to be collected and writes it off as a loss for accounting purposes typically after 180 days of delinquency. Conversely, collection refers to the active process of recovering outstanding debts through various communication channels and strategies. The critical insight for Collections Managers and CFOs is that a charged-off debt doesn't disappear; it simply transitions from one stage of the recovery process to another, often becoming more challenging and costly to recover.

According to the Philadelphia Fed Working Paper on Debt Collection Dynamics, understanding the efficacy differences between charge-off strategies and third-party collections is essential for optimizing recovery rates while managing compliance risks under the FDCPA.

This comprehensive guide examines the charge off vs collection debate from an operational perspective, providing actionable insights for directors and managers seeking to implement scalable, AI-powered solutions like those offered by AI debt collection platforms.

What Is a Charge-Off? Definition and Financial Implications

A charge-off is an accounting designation indicating that a creditor has moved a delinquent account from its active receivables to a loss category. This typically occurs after 120-180 days of non-payment, depending on the debt type and industry regulations. The NCUA Loan Charge-Off Policy Guidelines provide systematic guidance on charge-off procedures, including board-approved policies for credit unions and examples of high-probability loss loans.

The Charge-Off Timeline: When Debts Are Written Off

The standard charge-off timeline varies by debt type:

- Credit card debt: Typically charged off at 180 days of delinquency

- Auto loans: Usually charged off between 120-150 days

- Personal loans: Generally charged off at 120-180 days

- Medical debt: Often charged off after 90-180 days, depending on facility policies

Understanding these timelines is critical for Directors of Operations who must coordinate recovery efforts across multiple debt portfolios and optimize collection strategies before accounts reach charge-off status.

Financial and Accounting Impact of Charge-Offs

When a creditor charges off a debt, they're recognizing it as a loss on their balance sheet for tax and financial reporting purposes. However, this accounting designation doesn't eliminate the legal obligation of the debtor to repay. For CFOs managing accounts receivable departments, charge-offs represent:

- Immediate financial loss: Reduced assets and income recognition

- Tax deductions: Ability to claim the loss against taxable income

- Credit reporting impact: Severe negative mark on debtor's credit report lasting seven years

- Continued collection rights: Legal ability to pursue recovery through internal or third-party collections

The Fannie Mae DU Credit Report Analysis on Collections and Charge-Offs specifies different requirements based on property type, demonstrating how charge-offs impact mortgage lending decisions and requiring strategic payoff considerations.

What Is Collection? Active Debt Recovery Strategies

Collection represents the active, ongoing process of recovering outstanding debts through systematic communication with debtors. Unlike charge-offs, which are accounting designations, collections involve proactive strategies including phone calls, emails, SMS messaging, letters, and increasingly, AI-powered automated solutions.

The Three Stages of Debt Collection

Understanding the charge off vs collection relationship requires recognizing that collections occur in stages:

1. First-Party Collections (Internal): The original creditor attempts recovery using internal resources, typically for the first 60-120 days of delinquency. This stage focuses on maintaining customer relationships while encouraging payment through reminders and payment plan negotiations.

2. Third-Party Collections (External Agencies): If internal efforts fail, debts are often transferred or sold to specialized collection agencies. These agencies employ more aggressive tactics while remaining compliant with FDCPA regulations. Modern agencies leverage end-to-end collection solutions to maximize efficiency.

3. Legal Collections: When other methods fail, creditors may pursue legal action, obtaining judgments that allow wage garnishment or asset seizure. This represents the most expensive and time-consuming collection strategy.

Modern Collection Methods and Technologies

Collections Managers seeking to maximize recovery rates while minimizing operational costs are increasingly turning to technology-driven solutions:

- Traditional call centers: Labor-intensive with high per-contact costs

- Automated dialing systems: Increased contact volume but limited personalization

- Email and SMS campaigns: Lower cost but often lower engagement rates

- AI-powered conversational agents: Scalable, compliant, and personalized communication through inbound conversational AI

The strategic advantage of modern compliance-focused collection solutions lies in their ability to personalize communication at scale while maintaining strict adherence to FDCPA and TCPA regulations.

Charge Off vs Collection: Key Operational Differences

The fundamental distinction in the charge off vs collection debate centers on purpose, timing, and strategic approach. While charge-offs represent an accounting recognition of potential loss, collections represent active recovery efforts that can occur before, during, or after charge-off.

Timing and Sequence Considerations

Collections typically begin immediately upon delinquency often within 30 days of a missed payment. Charge-offs occur later, usually at 120-180 days. However, collection efforts don't stop at charge-off; they often intensify as accounts are transferred to specialized recovery teams or third-party agencies.

For Directors of Operations, this timeline distinction is crucial for resource allocation. Early-stage collections (pre-charge-off) typically yield higher recovery rates with lower effort, making them ideal candidates for automated accounts receivable solutions.

Financial Treatment and Reporting

The accounting treatment differs significantly:

| Aspect | Charge-Off | Collection |

|---|---|---|

| Balance Sheet Impact | Moved to loss category; reduces assets | Remains as active receivable |

| Income Recognition | Loss recognized immediately | Income recorded upon recovery |

| Tax Treatment | Deductible as bad debt expense | Recovered amounts treated as income |

| Credit Reporting | Reported as charge-off (severe impact) | Reported as collection account |

Legal Rights and Obligations

Both charge-offs and collections maintain the debtor's legal obligation to repay. The critical difference lies in enforcement strategy and regulatory compliance requirements. Collection activities are heavily regulated under the Fair Debt Collection Practices Act (FDCPA), requiring strict adherence to communication rules, disclosure requirements, and consumer rights protections.

Organizations implementing FDCPA-compliant AI debt collection strategies can maintain aggressive recovery efforts while automatically documenting compliance with every interaction.

Impact on Recovery Rates: Charge Off vs Collection Strategies

Recovery rate optimization is the primary concern for CFOs and Collections Managers evaluating the charge off vs collection decision. Research consistently shows that early intervention before charge-off yields significantly higher recovery rates.

Pre-Charge-Off Collection Effectiveness

Collections initiated within 30-60 days of delinquency typically achieve recovery rates of 60-80%, depending on debt type and debtor demographics. These early-stage efforts benefit from:

- Stronger customer relationships and communication channels

- Lower debtor financial distress (debt hasn't compounded significantly)

- Greater willingness to cooperate before credit damage occurs

- Lower operational costs per dollar recovered

Implementing promise-to-pay automation during this stage can dramatically improve conversion rates while reducing manual intervention requirements.

Post-Charge-Off Collection Challenges

Once an account reaches charge-off status, recovery rates typically drop to 15-30%. Contributing factors include:

- Debtor has already experienced severe credit damage, reducing cooperation incentive

- Account may have been sold to third-party agencies at steep discounts

- Debtor financial situation has likely deteriorated further

- Increased legal and operational costs per recovery attempt

However, specialized third-party agencies often achieve better results on charged-off accounts due to their expertise, technology, and dedicated focus. Modern agencies leverage batch calling automation to efficiently contact large volumes of charged-off accounts.

Regulatory Compliance in Charge Off vs Collection

Compliance considerations fundamentally shape the charge off vs collection strategy for risk-aware decision-makers. While charge-offs primarily involve accounting and reporting compliance, collections involve extensive consumer protection regulations.

FDCPA Requirements for Collection Activities

The Fair Debt Collection Practices Act strictly regulates third-party collection agencies, prohibiting:

- Contacting debtors at inconvenient times (before 8 AM or after 9 PM)

- Communicating with third parties about the debt

- Using threatening, abusive, or harassing language

- Misrepresenting the debt amount or legal status

- Continuing contact after written cease-and-desist requests

First-party creditors (collecting their own debts) face fewer restrictions but must still comply with general consumer protection laws. Organizations can ensure comprehensive compliance through AI-powered debt collection platforms that automatically document interactions and enforce regulatory boundaries.

TCPA and Communication Channel Regulations

The Telephone Consumer Protection Act adds another compliance layer, particularly for automated calling systems. Collections Managers implementing automated solutions must ensure:

- Prior express consent for automated calls to cell phones

- Proper identification in all communications

- Respect for do-not-call registrations

- Compliance with state-specific regulations

Modern omnichannel support platforms provide compliant communication across phone, SMS, email, and web channels while maintaining comprehensive audit trails.

AI-Powered Solutions: Optimizing Both Charge Off and Collection Strategies

The evolution of AI technology has fundamentally transformed the charge off vs collection calculus, enabling organizations to prevent charge-offs through early intervention while improving recovery rates on charged-off accounts.

Predictive Analytics for Charge-Off Prevention

AI-powered platforms analyze debtor behavior patterns, payment history, and demographic factors to identify high-risk accounts before they reach charge-off status. This enables:

- Proactive outreach to at-risk accounts

- Customized payment plan offerings based on predicted capacity to pay

- Resource allocation optimization focusing on accounts most likely to respond

- Early escalation of accounts requiring specialized intervention

Automated Collection for Maximum Efficiency

Directors of Operations seeking to replace or augment traditional call centers are implementing AI solutions that provide:

- 24/7 availability: Debtors can engage at their convenience, dramatically increasing contact rates

- Personalized communication: Natural language processing adapts messaging to individual debtor circumstances

- Multi-language support: Automated translation enables communication with diverse debtor populations

- Compliance automation: Every interaction is automatically documented and checked against regulatory requirements

Organizations implementing these solutions report significant improvements in both recovery rates and operational efficiency. The ROI comparison between generative AI and traditional debt collection demonstrates substantial cost savings and recovery improvements.

Self-Service Debt Resolution

Modern debtors increasingly prefer digital self-service options over traditional phone negotiations. Self-service debt resolution platforms enable debtors to:

- View account details and payment history

- Negotiate payment plans within pre-approved parameters

- Make immediate payments through secure portals

- Request hardship accommodations without agent interaction

This approach reduces operational costs while improving debtor satisfaction and payment conversion rates.

Industry-Specific Considerations: Charge Off vs Collection Across Sectors

The optimal balance between charge-off timing and collection strategy varies significantly across industries, requiring specialized approaches for different debt types.

Financial Services and Banking

Banks and credit unions face strict regulatory requirements for charge-off timing and collection practices. Financial service collection solutions must balance aggressive recovery efforts with customer relationship preservation, particularly for customers with multiple product relationships.

Healthcare Revenue Cycle Management

Medical debt presents unique challenges, including patient sensitivity, complex insurance interactions, and regulatory restrictions. Healthcare collection platforms must navigate HIPAA privacy requirements while maintaining compassionate communication approaches that preserve patient relationships.

Auto Finance Collections

Auto loans involve collateral considerations that fundamentally change the charge off vs collection equation. Auto finance collection strategies must coordinate repossession timing, asset valuation, and deficiency balance collection efforts.

Utilities and Telecommunications

Utility and telecom providers often have ongoing customer relationships that extend beyond individual debts. Utilities and telecom collection solutions must balance recovery efforts with service continuity and regulatory obligations.

Best Practices for Optimizing Charge Off vs Collection Strategies

Collections Managers and Directors of Operations can implement several best practices to optimize the charge off vs collection balance:

Implement Early Intervention Programs

Focus resources on preventing charge-offs through proactive communication at the first sign of delinquency. Automated systems can initiate contact within 24-48 hours of a missed payment, dramatically improving resolution rates.

Develop Account Segmentation Strategies

Not all delinquent accounts warrant the same level of effort. Segment accounts based on:

- Balance amount and potential recovery value

- Debtor payment history and creditworthiness

- Time since last payment

- Communication responsiveness

Invest in Scalable Technology Solutions

Traditional call center approaches cannot economically contact all delinquent accounts with sufficient frequency. AI-powered solutions provide unlimited scalability, enabling contact attempts that would be cost-prohibitive with human agents.

Maintain Compliance-First Approach

Regulatory violations can quickly negate recovery gains through penalties and reputational damage. Implement automated compliance checking and comprehensive documentation for every debtor interaction.

Leverage Data Analytics for Continuous Improvement

Track performance metrics across the entire debt lifecycle, identifying optimization opportunities in charge-off timing, collection channel effectiveness, and agent performance. Post-call analysis tools provide actionable insights for continuous refinement.

Measuring Success: KPIs for Charge Off and Collection Performance

CFOs and Directors of Operations require quantifiable metrics to evaluate charge off vs collection strategies:

Essential Performance Indicators

- Charge-off rate: Percentage of accounts reaching charge-off status (lower is better)

- Pre-charge-off recovery rate: Percentage of delinquent accounts resolved before charge-off

- Post-charge-off recovery rate: Percentage of charged-off balance ultimately recovered

- Days to resolution: Average time from delinquency to payment resolution

- Cost per dollar collected: Total collection costs divided by recovered amounts

- Right party contact rate: Percentage of contact attempts reaching the actual debtor (improved through right party verification)

- Promise-to-pay conversion rate: Percentage of debtor contacts resulting in payment commitments

- Promise-to-pay fulfillment rate: Percentage of payment commitments actually honored

Calculating ROI on Collection Technology Investments

When evaluating AI-powered collection solutions, calculate comprehensive ROI including:

- Increased recovery rates from improved contact frequency and personalization

- Reduced operational costs from automation of routine contacts

- Compliance risk reduction and associated penalty avoidance

- Improved charge-off prevention through earlier intervention

- Enhanced debtor satisfaction and relationship preservation

Future Trends: The Evolution of Charge Off and Collection Strategies

The debt collection industry is experiencing rapid transformation driven by technology advancement, regulatory evolution, and changing consumer expectations. Looking forward to 2026 and beyond:

Continued AI Advancement

Machine learning models will become increasingly sophisticated at predicting debtor behavior, optimal contact timing, and most effective communication strategies. Natural language processing will enable increasingly human-like conversations that debtors find less adversarial.

Omnichannel Integration

Debtors will engage across multiple channels phone, SMS, email, web chat, and portal with seamless continuity. Collection strategies will adapt in real-time based on debtor channel preferences and responsiveness patterns.

Regulatory Evolution

Collection regulations will continue evolving, with increased focus on consumer protection and transparency. Organizations with compliance-first technology platforms will maintain competitive advantages over those relying on manual processes.

Enhanced Payment Flexibility

Modern payment technologies will enable micro-payments, income-based dynamic payment schedules, and instant payment processing, reducing friction in the payment process and improving conversion rates.

Frequently Asked Questions About Charge Off vs Collection

Does a charge-off mean I no longer owe the debt?

No. A charge-off is an accounting designation by the creditor, not a cancellation of your legal obligation. The debt remains collectible, and creditors or collection agencies can continue pursuing payment.

Can a charged-off debt still be collected?

Yes. Charged-off debts can be collected by the original creditor, sold to debt buyers, or assigned to third-party collection agencies. Collection rights typically persist until the statute of limitations expires, which varies by state and debt type.

Which hurts credit more: charge-off or collection?

Both significantly damage credit scores, but charge-offs are generally considered more severe. A charge-off indicates the creditor has given up on collection, while a collection account suggests ongoing recovery efforts.

How long do charge-offs and collections stay on credit reports?

Both remain on credit reports for seven years from the date of first delinquency, regardless of whether the debt is eventually paid.

Should I pay a charged-off debt?

Paying a charged-off debt eliminates the legal obligation and stops collection efforts, but won't remove the charge-off from your credit report. However, it will be updated to show 'paid charge-off,' which is marginally better for creditworthiness.

Can AI improve collection rates on charged-off accounts?

Yes. AI-powered collection platforms dramatically improve contact rates, personalize communication strategies, and enable 24/7 engagement, significantly improving recovery rates even on aged, charged-off accounts.

Conclusion

Understanding the distinction between charge off vs collection is essential for decision-makers seeking to optimize debt recovery operations. While charge-offs represent accounting recognition of potential loss, collections represent active recovery strategies that can occur throughout the debt lifecycle before, during, and after charge-off designation.

Modern AI-powered solutions are transforming both aspects of debt recovery, enabling early intervention that prevents charge-offs while improving recovery rates on charged-off accounts. For Collections Managers, Directors of Operations, and CFOs focused on maximizing recovery rates while minimizing operational costs and ensuring regulatory compliance, implementing scalable, automated solutions represents the optimal path forward. By leveraging technology to personalize communication, maintain compliance, and enable self-service resolution, organizations can fundamentally improve their debt recovery performance across all stages of the collection lifecycle.

Ready to Transform Your Collections Process?

See how CollectDebt.ai can help you automate debt collection, reduce costs, and improve compliance.