AI Debt Collection: The Complete 2026 Guide To Automated Recovery Solutions

The debt collection industry is undergoing a dramatic transformation as artificial intelligence reshapes how organizations recover outstanding accounts. AI debt collection combines machine learning, natural language processing, and predictive analytics to create smarter, more effective recovery strategies that benefit both creditors and consumers. This comprehensive guide explores how AI-powered solutions are revolutionizing the collections landscape in 2026 and beyond.

Understanding AI Debt Collection

AI debt collection refers to the application of artificial intelligence technologies to automate and optimize the debt recovery process. Unlike traditional methods that rely heavily on manual dialing, scripted conversations, and generic outreach strategies, AI debt collection systems leverage sophisticated algorithms to personalize every interaction, predict debtor behavior, and maximize recovery rates while maintaining regulatory compliance.

Modern AI debt collection solutions integrate multiple technologies including conversational AI, voice recognition, sentiment analysis, and intelligent routing to create seamless, respectful debtor experiences. These systems can handle thousands of simultaneous conversations, adapt messaging based on real-time responses, and identify the optimal communication channels for each individual account.

The shift toward AI-powered collections represents more than just technological advancement it fundamentally changes the economics and ethics of debt recovery. By removing human bias, reducing operational costs, and enabling more empathetic interactions, AI debt collection creates a win-win scenario where creditors recover more funds while debtors receive more flexible, respectful treatment.

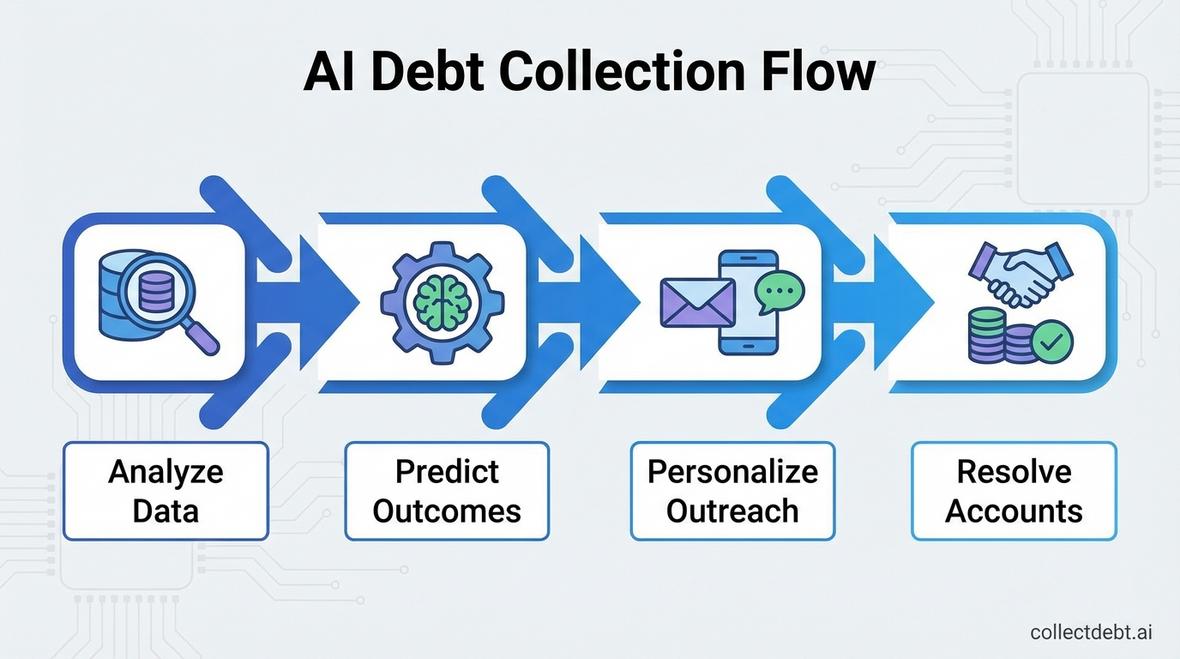

How AI Debt Collection Works: The Four-Step Process

The AI debt collection workflow consists of four interconnected stages that transform raw account data into successful resolutions. Understanding this process helps organizations appreciate the sophistication behind modern recovery systems.

Step 1: Analyze Data

The foundation of effective AI debt collection begins with comprehensive data analysis. Advanced systems ingest information from multiple sources including account histories, payment patterns, demographic data, previous communication logs, and external credit bureau information. Machine learning algorithms process these datasets to identify meaningful patterns and segment accounts based on likelihood to pay, preferred communication channels, and risk profiles.

This analytical phase goes far beyond simple credit scoring. Modern AI systems examine hundreds of variables simultaneously, identifying subtle correlations that human analysts would never detect. For example, the system might discover that debtors in specific zip codes respond better to SMS messages sent on Tuesday mornings, or that accounts with certain employment histories are more likely to honor payment arrangements made during the first week of the month.

Step 2: Predict Outcomes

Once data analysis is complete, predictive models forecast the probable outcomes for each account. These algorithms calculate the optimal contact strategy, estimate the likelihood of payment at various proposed amounts, and determine which offers are most likely to result in successful resolution. According to research from leading analytics firms, predictive modeling can improve recovery rates by 15-30% compared to traditional approaches.

The prediction engine also identifies accounts that require special handling those at high risk of dispute, those eligible for hardship programs, or those likely to respond to self-service debt resolution options. This intelligent triage ensures that human collectors focus their efforts on accounts where their expertise adds the most value.

Step 3: Personalize Outreach

Armed with predictive insights, AI debt collection systems craft personalized outreach campaigns tailored to each debtor's unique circumstances. Omnichannel support enables seamless communication across voice, SMS, email, and digital portals, meeting debtors where they prefer to engage.

Conversational AI agents conduct natural, empathetic dialogues that adapt in real-time based on debtor responses. If a debtor expresses financial hardship, the system automatically offers flexible payment arrangements. If they dispute the debt, the conversation shifts to validation procedures. This dynamic personalization creates more productive interactions that feel respectful rather than adversarial.

The personalization extends to timing as well. AI systems identify the optimal contact cadence for each account, avoiding over-communication that leads to complaints while maintaining sufficient touchpoints to drive action. Advanced right party verification ensures that every conversation reaches the correct individual, reducing compliance risks and improving efficiency.

Step 4: Resolve Accounts

The final stage brings accounts to successful closure through a combination of automated and human-assisted processes. AI systems facilitate promise to pay arrangements, process payments through integrated payment gateways, and automatically update account statuses across connected systems.

For complex situations requiring human intervention, the AI provides collectors with comprehensive briefings including conversation history, recommended strategies, and predicted outcomes. This agent assist approach amplifies human capabilities rather than replacing them, creating a hybrid model that combines AI efficiency with human judgment.

Key Benefits of AI Debt Collection

Organizations implementing AI debt collection systems realize transformative benefits across operational, financial, and compliance dimensions. These advantages explain why adoption rates continue accelerating throughout 2026.

Increased Recovery Rates

The most compelling benefit of AI debt collection is improved recovery performance. Industry data shows that AI-powered systems consistently outperform traditional methods by 20-40% across diverse portfolio types. This improvement stems from better contact rates, more effective messaging, optimized payment arrangements, and reduced account aging.

Personalized communication strategies resonate more effectively with debtors, increasing their willingness to engage and resolve obligations. Predictive analytics identify the optimal settlement amounts that balance debtor capacity with creditor recovery goals, maximizing the probability of successful collection.

Reduced Operational Costs

Automation dramatically reduces the cost per dollar collected. AI debt collection systems handle routine accounts without human intervention, allowing organizations to scale collection capacity without proportional increases in staffing. According to operational benchmarks, AI-powered collections can reduce per-account handling costs by 50-70% compared to traditional call center models.

These savings extend beyond direct labor costs. AI systems eliminate training expenses for high-turnover collector positions, reduce facility requirements, and minimize the compliance infrastructure needed to monitor human agent interactions. The capital freed by these efficiencies can be reinvested in technology improvements or returned to stakeholders.

Enhanced Compliance

Regulatory compliance represents one of the most challenging aspects of debt collection. The Fair Debt Collection Practices Act and similar regulations impose strict requirements on communication timing, frequency, content, and documentation. Human collectors, despite best intentions, occasionally make mistakes that expose organizations to costly litigation.

AI systems eliminate compliance risks by programming regulatory requirements directly into their decision logic. Every communication automatically adheres to FDCPA compliance standards, calls occur only during permitted hours, contact frequency respects legal limits, and all interactions are comprehensively documented. Post-call analysis provides additional quality assurance by automatically reviewing conversations for potential compliance issues.

Improved Debtor Experience

While creditor benefits often receive primary attention, AI debt collection significantly improves experiences for debtors as well. Conversational AI agents communicate with empathy and patience, never displaying frustration or judgment regardless of how many times a debtor changes their mind or asks questions.

Self-service options empower debtors to resolve obligations on their own schedules without the stress of live conversations. Flexible payment arrangements accommodate individual financial situations, and multilingual capabilities ensure that language barriers never prevent someone from accessing assistance. This respectful, accessible approach reduces the shame and anxiety traditionally associated with collections, making debtors more willing to engage productively.

Industry-Specific Applications of AI Debt Collection

Different sectors face unique collection challenges that require tailored approaches. AI debt collection systems adapt to industry-specific requirements while maintaining core capabilities.

Healthcare Collections

Medical debt represents one of the most sensitive collection categories, requiring exceptional empathy and flexibility. Healthcare AI debt collection systems recognize this sensitivity and adjust communication strategies accordingly. These solutions integrate with billing systems to explain complex medical charges, offer financial assistance program screening, and facilitate payment plans that align with patient financial capacity.

Early-stage early out self-pay healthcare collections benefit particularly from AI automation, which can engage patients before accounts become severely delinquent, preserving the patient-provider relationship while improving recovery rates.

Auto Finance Collections

The auto finance industry leverages AI debt collection to manage secured loan portfolios more effectively. Predictive models assess repossession risk, enabling proactive outreach before accounts reach critical delinquency stages. AI systems coordinate with borrowers to arrange catch-up payments, refinancing options, or voluntary surrenders when appropriate.

Vehicle location data, payment history analytics, and economic indicators combine to create comprehensive risk profiles that inform collection strategies. This intelligence allows lenders to balance recovery objectives with borrower retention, particularly for customers with strong long-term value.

Utilities and Telecommunications

Subscription-based services in the utilities and telecom sectors use AI debt collection to manage high-volume, relatively low-balance accounts efficiently. Automated systems handle routine late payments while identifying patterns that indicate financial distress versus simple oversight.

For customers experiencing genuine hardship, AI systems automatically offer assistance programs, payment extensions, or reduced service tiers that maintain connectivity while accommodating temporary financial constraints. This approach reduces involuntary churn while maintaining revenue collection.

Financial Services

Banks and financial service providers deploy AI debt collection across diverse product lines including credit cards, personal loans, and lines of credit. Sophisticated segmentation enables differentiated strategies for prime versus subprime portfolios, recent customers versus long-tenured relationships, and secured versus unsecured obligations.

Integration with broader customer relationship management systems ensures that collection activities coordinate with retention efforts, cross-sell opportunities, and overall customer lifetime value optimization. This holistic approach prevents collections from damaging valuable banking relationships unnecessarily.

Implementing AI Debt Collection: Key Considerations

Organizations considering AI debt collection adoption should evaluate several critical factors to ensure successful implementation and optimal return on investment.

Integration Requirements

Effective AI systems require seamless connectivity with existing technology infrastructure including collection management systems, payment processors, customer databases, and communication platforms. Robust integration capabilities determine how quickly organizations can deploy AI solutions and realize value.

APIs, webhooks, and pre-built connectors for popular platforms accelerate implementation timelines. Organizations should prioritize solutions offering flexible integration options that accommodate both modern cloud-based systems and legacy on-premise infrastructure.

Data Quality and Preparation

AI systems are only as effective as the data they process. Before implementation, organizations should audit existing data for completeness, accuracy, and consistency. Missing phone numbers, outdated addresses, and inconsistent account coding undermine AI performance just as they handicap traditional collection methods.

Data enrichment services can supplement internal records with additional contact information, skip tracing results, and enhanced demographic profiles. This augmented dataset enables more sophisticated segmentation and personalization from day one.

Change Management and Training

Introducing AI debt collection represents significant organizational change that affects collectors, compliance teams, IT departments, and leadership. Successful implementations require comprehensive change management programs that address concerns, communicate benefits, and provide adequate training.

Collectors may fear displacement by automation. Effective programs reposition AI as a tool that eliminates tedious work and amplifies human capabilities rather than replacing people entirely. Training focuses on new skills like AI oversight, exception handling, and complex negotiation for escalated accounts.

Vendor Selection Criteria

The AI debt collection marketplace includes numerous vendors with varying capabilities, specializations, and business models. Organizations should evaluate potential partners across multiple dimensions including technology sophistication, industry experience, compliance expertise, implementation support, and ongoing service quality.

Proof-of-concept pilots allow organizations to assess performance with their specific portfolio characteristics before committing to full-scale deployment. Reference checks with existing customers provide insights into post-sale support quality and long-term partnership satisfaction.

Future Trends in AI Debt Collection

The AI debt collection landscape continues evolving rapidly as new technologies emerge and regulatory frameworks adapt. Several trends will shape the industry throughout 2026 and beyond.

Hyper-Personalization Through Advanced NLP

Natural language processing capabilities continue advancing, enabling even more nuanced, context-aware conversations. Future AI systems will detect subtle emotional cues in debtor responses, adjusting tone, pacing, and content in real-time to optimize engagement and resolution probability.

Sentiment analysis will identify frustration, confusion, or distress early in conversations, triggering appropriate responses such as simplified explanations, supervisor escalation, or hardship program offers. This emotional intelligence creates interactions that feel genuinely empathetic rather than mechanically scripted.

Predictive Delinquency Prevention

The most effective collection is preventing delinquency before it occurs. Advanced analytics platforms now identify at-risk accounts based on payment pattern changes, life event indicators, and economic conditions. Proactive outreach offering payment plan modifications, temporary forbearance, or financial counseling resources helps borrowers stay current rather than falling behind.

This shift from reactive collection to proactive relationship management transforms the debt collection function into a customer success initiative that supports long-term account performance while reducing eventual charge-off losses.

Regulatory Technology Integration

As regulations governing debt collection continue evolving, AI systems will incorporate regulatory technology (RegTech) capabilities that automatically adapt to new requirements. When state-level regulations change, compliant AI systems will update their operating parameters immediately without manual reprogramming.

Blockchain-based audit trails may provide immutable documentation of all collection activities, simplifying compliance verification and dispute resolution. Smart contracts could automatically enforce regulatory constraints at the system architecture level, making non-compliance technically impossible rather than merely prohibited.

Frequently Asked Questions About AI Debt Collection

Does AI debt collection completely replace human collectors?

No, effective AI debt collection creates a hybrid model where automation handles routine accounts while human collectors focus on complex situations requiring judgment, negotiation skills, and emotional intelligence. This division of labor maximizes efficiency while preserving the human touch for accounts that benefit from it.

How does AI ensure compliance with debt collection regulations?

AI systems encode regulatory requirements directly into their decision logic, automatically adhering to contact time restrictions, frequency limits, disclosure requirements, and communication standards. Every interaction is documented comprehensively, and compliance monitoring tools continuously audit system behavior to identify and correct any deviations.

What is the typical cost of implementing AI debt collection?

Implementation costs vary widely based on portfolio size, integration complexity, and deployment model. Cloud-based solutions typically operate on per-account or percentage-of-recovery pricing models that align vendor compensation with client results. Organizations should expect initial setup investments for integration and configuration, followed by ongoing operational costs that remain substantially lower than traditional collection methods.

How quickly can organizations see ROI from AI debt collection?

Most organizations realize positive return on investment within 3-6 months of deployment. Recovery rate improvements and operational cost reductions typically generate savings that exceed implementation costs relatively quickly. The exact timeline depends on portfolio characteristics, previous collection performance, and implementation approach.

Which industries benefit most from AI debt collection?

Virtually every industry with accounts receivable can benefit from AI debt collection, but sectors with high-volume, relatively standardized accounts see the fastest returns. Healthcare, utilities, telecommunications, financial services, and retail organizations have led adoption, though industries like real estate and hospitality are increasingly implementing AI solutions as well.

Conclusion

AI debt collection represents a fundamental transformation in how organizations manage accounts receivable and recover outstanding obligations. By combining predictive analytics, conversational AI, and intelligent automation, modern systems achieve recovery rates that exceed traditional methods while reducing costs and improving debtor experiences. As we progress through 2026, organizations that embrace AI debt collection gain competitive advantages through operational efficiency, regulatory compliance, and enhanced customer relationships. Whether you operate in healthcare, financial services, utilities, or any other sector with collection needs, AI-powered solutions offer compelling benefits that justify serious evaluation. The future of debt collection is intelligent, empathetic, and automated and that future is already here.

Ready to Transform Your Collections Process?

See how CollectDebt.ai can help you automate debt collection, reduce costs, and improve compliance.