FDCPA Compliant AI Debt Collection Software: The Complete Guide For Collection Agencies

The debt collection industry stands at a critical inflection point. As regulatory scrutiny intensifies and consumer expectations evolve, collection agencies and accounts receivable departments must adopt technology that simultaneously enhances recovery rates and ensures ironclad compliance. FDCPA compliant AI debt collection software has emerged as the definitive solution for organizations seeking to modernize operations while navigating the complex regulatory landscape defined by the Fair Debt Collection Practices Act and related statutes.

For Directors of Operations, Collections Managers, and CFOs overseeing debt recovery operations, understanding how artificial intelligence can transform collection workflows without exposing the organization to legal risk is no longer optional. This comprehensive guide examines the essential features, regulatory considerations, and quantifiable benefits of implementing FDCPA compliant AI debt collection software in 2026 and beyond.

Understanding FDCPA Compliance in the AI Era

The Fair Debt Collection Practices Act (FDCPA) establishes foundational rules governing how third-party debt collectors may interact with consumers. These regulations prohibit harassment, false statements, unfair practices, and impose strict limits on communication frequency and timing. For decades, compliance depended primarily on training human collectors and implementing manual oversight processes an approach that introduced significant variability and risk.

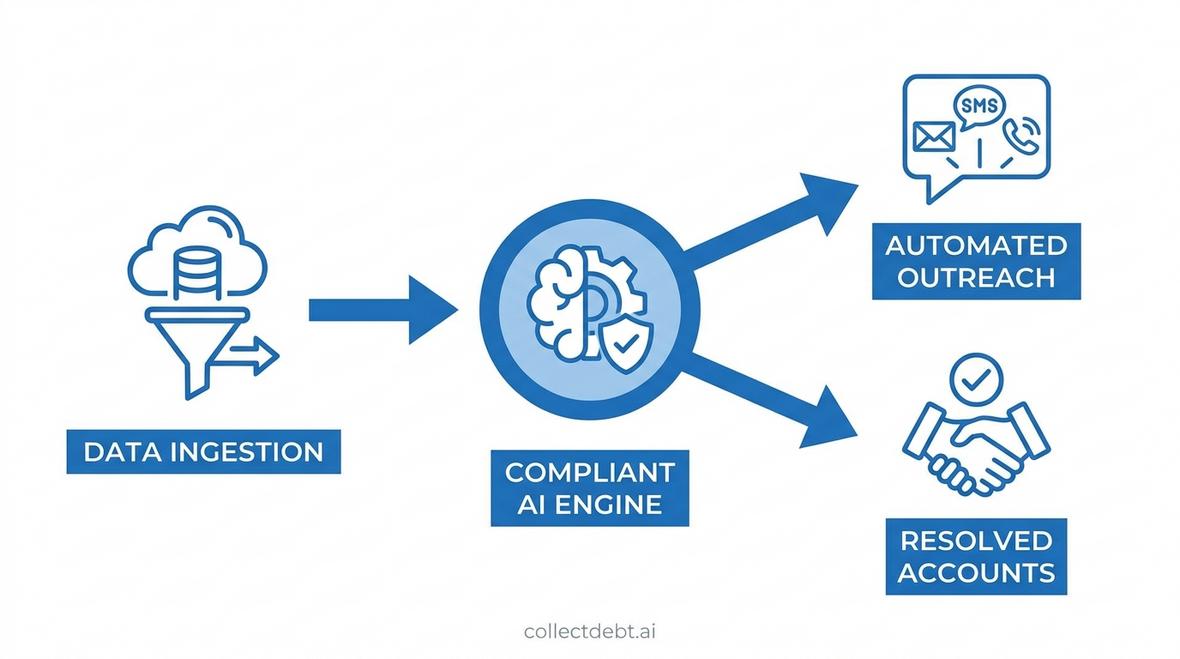

Modern FDCPA compliant AI debt collection software fundamentally reimagines compliance by embedding regulatory constraints directly into automated workflows. Rather than relying on individual collector judgment, these platforms enforce rules programmatically, ensuring every consumer interaction adheres to federal and state requirements regardless of volume or complexity.

Regulation F: The New Compliance Paradigm

The Consumer Financial Protection Bureau's Regulation F codifies specific numerical limits that dramatically impact collection operations. The regulation establishes the '7-in-7' rule, prohibiting collectors from attempting telephone conversations with consumers more than seven times within seven consecutive days regarding a specific debt. Additionally, Regulation F mandates precise validation notice content and prescribes safe harbor language for written communications.

These quantitative restrictions are particularly well-suited to AI enforcement. Leading FDCPA compliant AI debt collection software platforms automatically track contact attempts across all channels, maintain rolling seven-day windows for each debt, and prevent system-initiated outreach that would violate call frequency limits. This programmatic compliance eliminates the manual tracking burden that previously consumed significant staff resources while reducing regulatory exposure.

Core Features of FDCPA Compliant AI Debt Collection Software

Not all AI collection platforms deliver genuine FDCPA compliance. Organizations evaluating solutions must scrutinize specific capabilities that differentiate compliant systems from generic automation tools. The following features represent non-negotiable requirements for any platform claiming FDCPA compliant AI debt collection software status.

Automated Communication Governance

Effective compliance solutions incorporate real-time communication governance that prevents prohibited contact before it occurs. This includes:

- Time-zone aware calling windows: Automatic enforcement of FDCPA-permitted calling hours (typically 8 AM to 9 PM in the consumer's local time zone) with dynamic adjustments for daylight saving time transitions

- Contact frequency limits: Systematic tracking of all communication attempts across phone, SMS, email, and other channels to enforce the 7-in-7 rule and any applicable state-specific restrictions

- Cease-and-desist processing: Immediate flagging and communication suppression when consumers invoke their right to stop contact, with workflow routing to ensure proper legal handling

- Third-party disclosure prevention: AI-driven verification protocols that confirm debtor identity before discussing debt details, protecting against unauthorized third-party disclosures

Intelligent Validation Notice Delivery

Regulation F requires debt collectors to provide a detailed validation notice within five days of initial communication. FDCPA compliant AI debt collection software automates this critical requirement by generating compliant notices immediately upon first contact, tracking delivery confirmation, and maintaining auditable records of all validation communications. Advanced platforms incorporate model validation notice language that satisfies safe harbor provisions while allowing customization for specific debt types or jurisdictions.

Right-Party Verification and Voice Authentication

One of the most significant compliance risks in automated collection involves confirming debtor identity before disclosing sensitive information. Modern right-party verification systems leverage voice biometrics, knowledge-based authentication, and conversational AI to establish identity with high confidence levels before proceeding with collection discussions. This technology dramatically reduces third-party disclosure risk compared to traditional verification methods while improving contact rates.

Omnichannel Compliance Orchestration

Contemporary consumers expect to engage across multiple channels phone, SMS, email, chat, and self-service portals. However, FDCPA compliance requirements apply differently across these modalities, and contact frequency limits aggregate across all channels. Leading omnichannel support platforms maintain unified consumer profiles that track all interaction history regardless of channel, apply channel-specific compliance rules, and orchestrate optimal outreach sequences that maximize engagement while maintaining regulatory boundaries.

Quantifying the ROI of FDCPA Compliant AI Debt Collection Software

Financial decision-makers evaluating FDCPA compliant AI debt collection software require concrete data on expected returns. While specific results vary based on portfolio characteristics and implementation scope, industry benchmarks and operational economics provide clear guidance on potential value.

Labor Cost Reduction and Efficiency Gains

According to Bureau of Labor Statistics data, the median annual wage for bill and account collectors exceeds $41,000, translating to approximately $20 per hour before benefits and overhead. When factoring in employer costs for benefits, workspace, technology, and management, the fully loaded cost per collector FTE typically ranges from $50,000 to $70,000 annually.

FDCPA compliant AI debt collection software enables a single collections professional to manage substantially larger portfolios by automating routine outreach, payment processing, and follow-up activities. Organizations implementing comprehensive AI solutions commonly report 3-5x improvements in accounts managed per FTE, effectively reducing per-account collection costs by 60-80% compared to traditional manual operations.

Recovery Rate Improvements Through Intelligent Engagement

Beyond cost reduction, advanced AI debt collection platforms demonstrably improve recovery rates through data-driven engagement optimization. AI systems analyze historical payment behavior, communication preferences, and debtor circumstances to determine optimal contact timing, channel selection, and messaging strategies for each individual account.

Industry implementations of FDCPA compliant AI debt collection software report liquidation rate improvements ranging from 15% to 40% compared to baseline manual collection performance. For an agency managing a $50 million portfolio, even a conservative 20% improvement in recovery rates represents $10 million in additional collections annually a transformative impact on agency economics and client relationships.

Compliance Risk Mitigation and Litigation Avoidance

FDCPA violations expose collection agencies to significant financial penalties. Individual consumers can recover actual damages plus statutory damages up to $1,000 per violation, with class action lawsuits potentially resulting in catastrophic settlements. Beyond direct legal costs, FDCPA litigation generates reputational damage, client attrition, and increased regulatory scrutiny that can threaten agency viability.

Programmatic compliance enforcement through FDCPA compliant AI debt collection software dramatically reduces violation frequency by eliminating human error and ensuring consistent rule application across all consumer interactions. Organizations implementing comprehensive AI compliance systems report 70-90% reductions in consumer complaints and regulatory inquiries, translating to substantial legal cost savings and risk mitigation.

Implementation Considerations for Collection Agencies

Successful deployment of FDCPA compliant AI debt collection software requires careful planning and execution. Organizations should address several critical considerations during evaluation and implementation phases.

Integration with Existing Collection Systems

Most collection agencies operate established technology stacks including collection management systems, dialers, payment processors, and CRM platforms. Effective integration capabilities determine whether AI solutions complement existing infrastructure or require disruptive wholesale replacements. Leading platforms offer pre-built connectors for major collection software vendors, RESTful APIs for custom integration, and real-time data synchronization that maintains consistent consumer records across systems.

Training and Change Management

Introducing AI-powered automation fundamentally changes collector roles, shifting focus from high-volume manual outreach to exception handling, complex negotiation, and relationship management. Successful implementations invest substantially in collector training, clearly communicate how AI augments rather than replaces human expertise, and redesign compensation structures to reward outcomes rather than activity volume.

Portfolio Segmentation and Hybrid Strategies

Not all accounts benefit equally from automated collection approaches. High-balance accounts, complex dispute situations, and legally sensitive cases often require human expertise and judgment. Sophisticated end-to-end collection solutions enable granular portfolio segmentation, routing lower-balance, straightforward accounts to fully automated AI workflows while reserving human collector capacity for high-value, complex situations that justify the additional cost.

Industry-Specific Applications of FDCPA Compliant AI

While FDCPA compliance requirements apply universally, different industries present unique collection challenges that influence optimal AI implementation strategies.

Healthcare Collections

Medical debt collection faces heightened sensitivity due to privacy regulations, patient relationships, and the emotional context surrounding healthcare services. Healthcare-focused AI collection platforms incorporate HIPAA compliance alongside FDCPA requirements, offer empathetic communication strategies calibrated for medical debt contexts, and integrate with electronic health record systems to maintain comprehensive patient financial profiles.

Financial Services and Consumer Lending

Banks, credit unions, and consumer finance companies managing financial services collections benefit from AI platforms that seamlessly transition accounts across internal recovery stages before external placement. These solutions maintain institutional voice and branding throughout the collection lifecycle, preserve customer relationships where possible, and provide detailed analytics on delinquency drivers that inform upstream credit decision improvements.

Auto Finance and Asset-Secured Lending

Collections on secured debts involve unique considerations around repossession rights, redemption opportunities, and deficiency balances. Auto finance collection platforms track collateral status, automate pre-repossession notification requirements, and coordinate with repossession agents while maintaining FDCPA compliance throughout the recovery process.

Selecting the Right FDCPA Compliant AI Debt Collection Software

The market for AI-powered collection technology has expanded rapidly, with numerous vendors claiming compliance capabilities. Organizations should evaluate platforms against specific criteria to identify solutions that deliver genuine regulatory protection and operational value.

Essential Evaluation Criteria

When assessing FDCPA compliant AI debt collection software options, decision-makers should prioritize:

- Regulatory expertise: Vendor demonstration of deep FDCPA knowledge, active monitoring of regulatory developments, and systematic platform updates reflecting rule changes

- Audit trail completeness: Comprehensive logging of all system decisions, consumer interactions, and compliance checkpoints with tamper-proof storage suitable for regulatory examination

- Configurability: Flexibility to implement custom compliance rules reflecting state-specific requirements, client preferences, and internal policies beyond minimum FDCPA standards

- Vendor stability: Financial health, client retention rates, and investment in ongoing platform development ensuring long-term partnership viability

- Implementation support: Structured onboarding methodology, dedicated implementation resources, and post-launch optimization assistance

Platform Comparison and Market Options

Organizations frequently compare multiple vendors during evaluation processes. Resources like platform comparison guides provide structured frameworks for assessing competing solutions across compliance capabilities, feature sets, pricing models, and integration requirements. When evaluating options, prioritize platforms purpose-built for debt collection over generic AI communication tools that lack collection-specific compliance engineering.

The Future Regulatory Landscape for AI Collections

Regulatory frameworks governing debt collection continue evolving in response to technological advancement and consumer protection priorities. Organizations implementing FDCPA compliant AI debt collection software must anticipate future regulatory developments and select platforms architected for adaptability.

State-Level Compliance Requirements

While FDCPA establishes federal baseline protections, numerous states impose additional restrictions on collection practices. California's Rosenthal Act, New York's debt collection regulations, and various state-specific statutes create a complex compliance matrix that varies by debtor location. Advanced AI platforms maintain jurisdiction-specific rule libraries and automatically apply the most restrictive applicable requirements to each consumer interaction.

Emerging AI Governance Frameworks

As artificial intelligence assumes greater roles in consumer-facing processes, regulators increasingly scrutinize AI decision-making for bias, transparency, and fairness. Forward-looking FDCPA compliant AI debt collection software incorporates explainable AI principles, bias testing protocols, and transparent decision logic that withstands regulatory examination while maintaining operational effectiveness.

Measuring Success: KPIs for AI Collection Programs

Implementing FDCPA compliant AI debt collection software requires establishing clear success metrics that balance financial performance, compliance objectives, and operational efficiency.

Financial Performance Metrics

Core financial KPIs for AI collection programs include:

- Liquidation rate: Percentage of portfolio value recovered, segmented by account age, balance range, and collection strategy

- Cost per dollar collected: Total collection costs (technology, labor, legal) divided by gross collections, tracking efficiency improvements over time

- Right-party contact rate: Percentage of outreach attempts resulting in verified debtor contact, measuring targeting accuracy

- Promise-to-pay conversion: Rate at which consumer contacts result in payment commitments, indicating communication effectiveness

Compliance and Quality Metrics

Equally important are compliance indicators that validate regulatory adherence:

- FDCPA violation rate: Consumer complaints alleging violations per thousand accounts worked, targeting zero or near-zero levels

- Cease-and-desist compliance: Percentage of stop-contact requests processed within required timeframes with zero subsequent unauthorized contact

- Call frequency compliance: Systematic verification that no accounts received contact attempts exceeding 7-in-7 limits or other applicable restrictions

- Validation notice delivery: Confirmation that 100% of initial communications trigger compliant validation notices within five-day windows

Platforms offering robust post-call analysis capabilities enable continuous compliance monitoring through AI-powered interaction review, automatically flagging potential issues for human examination and creating feedback loops that improve system performance.

Getting Started with FDCPA Compliant AI Debt Collection Software

Organizations ready to explore FDCPA compliant AI debt collection software should approach implementation systematically, beginning with clear objectives and progressing through structured evaluation and deployment phases.

Pilot Program Design

Rather than enterprise-wide deployment, successful implementations typically begin with focused pilot programs targeting specific portfolio segments. Ideal pilot populations include:

- Lower-balance accounts where manual collection economics are challenged

- Specific debt types with standardized characteristics (medical bills, utility arrears, retail accounts)

- Geographic regions enabling state-specific compliance testing

- Accounts in early delinquency stages where AI-driven early intervention shows particular promise

Pilot programs should run for sufficient duration (typically 90-180 days) to generate statistically significant performance data while maintaining parallel manual collection workflows for comparison and fallback protection.

Vendor Partnership and Support

The relationship between collection agencies and AI platform providers extends far beyond software licensing. Successful deployments require genuine partnership characterized by:

- Collaborative configuration reflecting agency-specific compliance policies and operational workflows

- Ongoing training ensuring staff competency with evolving platform capabilities

- Regular business reviews analyzing performance data and identifying optimization opportunities

- Proactive regulatory updates as compliance requirements change

Organizations should evaluate vendor commitment to long-term partnership during selection processes, prioritizing providers with demonstrated client success programs and responsive support infrastructure.

Frequently Asked Questions

What does FDCPA compliant AI debt collection software cost?

Pricing models vary significantly across vendors, typically structured as per-account fees, per-contact pricing, or percentage-of-collections arrangements. Enterprise implementations generally range from $15,000 to $150,000+ annually depending on portfolio size, feature requirements, and integration complexity. Organizations should evaluate total cost of ownership including implementation services, training, and ongoing support rather than focusing exclusively on licensing fees.

Can AI completely replace human debt collectors?

While FDCPA compliant AI debt collection software automates substantial collection activity, complete human replacement remains neither advisable nor practical. High-value accounts, complex disputes, legal proceedings, and situations requiring nuanced judgment continue to benefit from experienced human collectors. Optimal implementations create hybrid models where AI handles high-volume routine interactions while human expertise focuses on complex, high-value situations.

How long does implementation typically take?

Implementation timelines vary based on integration complexity, data migration requirements, and customization scope. Organizations with modern, API-enabled technology stacks can achieve basic implementations in 4-8 weeks, while complex environments requiring extensive custom integration may extend to 3-6 months. Phased rollouts beginning with pilot programs offer faster initial deployment while managing implementation risk.

Does AI software handle state-specific compliance requirements?

Leading FDCPA compliant AI debt collection software platforms maintain comprehensive libraries of state-specific collection regulations and automatically apply jurisdiction-appropriate rules based on debtor location. However, organizations must verify that specific state requirements relevant to their operations are supported and properly configured during implementation.

Conclusion

The convergence of artificial intelligence and debt collection represents a transformative opportunity for agencies seeking to enhance recovery performance while maintaining ironclad regulatory compliance. FDCPA compliant AI debt collection software delivers quantifiable improvements in liquidation rates, operational efficiency, and compliance risk mitigation benefits that directly impact agency profitability and competitive positioning. As regulatory complexity increases and consumer expectations evolve, organizations that strategically implement AI-powered collection technology position themselves for sustained success in an increasingly challenging market. Decision-makers should begin evaluation processes now, engaging with proven platforms like CollectDebt.ai that combine deep regulatory expertise with cutting-edge AI capabilities to deliver compliant, effective, and scalable collection solutions.

Ready to Transform Your Collections Process?

See how CollectDebt.ai can help you automate debt collection, reduce costs, and improve compliance.