Arkansas Statute Of Limitations On Debt Collection: Complete 2026 Guide For Collection Agencies

Understanding the Arkansas Statute of Limitations on Debt Collection

The arkansas statute of limitations on debt collection establishes critical legal boundaries that govern how long creditors and collection agencies can pursue unpaid debts through the court system. For collection managers, compliance officers, and financial decision-makers operating in Arkansas, understanding these statutory time limits is essential for maintaining regulatory compliance while maximizing recovery rates.

Arkansas law establishes specific timeframes during which creditors can file lawsuits to collect various types of debt. Once the statute of limitations expires, the debt becomes 'time-barred,' meaning creditors lose their legal right to sue for collection though the debt itself doesn't disappear. For debt collection agencies leveraging AI-powered debt collection solutions, understanding these limitations ensures compliant, effective recovery strategies that protect both the organization and consumers.

According to Arkansas state agency FAQs on debt collection time limitations, Arkansas maintains stringent protections against creditors attempting to pursue collection efforts beyond statutory time limits. This regulatory framework requires collection operations to implement sophisticated tracking systems that monitor debt age and ensure all collection activities remain within legal boundaries.

Arkansas Statute of Limitations by Debt Type

The arkansas statute of limitations on debt collection varies significantly depending on the type of debt involved. Understanding these distinctions is fundamental for collection agencies structuring their portfolios and prioritizing recovery efforts.

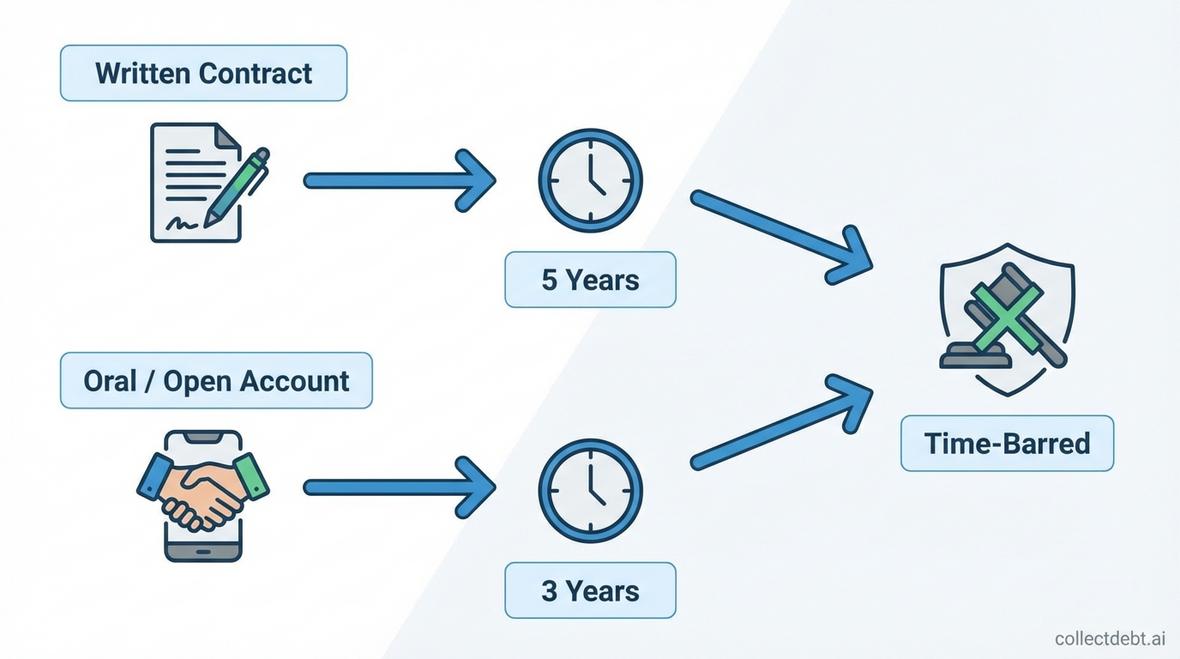

Written Contracts: Five-Year Limitation Period

For debts arising from written contracts including credit card agreements with written terms, personal loans with signed documentation, auto loans, and mortgage agreements Arkansas establishes a five-year statute of limitations. This means creditors have five years from the date of default or last payment to initiate legal action for debt recovery.

Written contracts provide the longest protection period for creditors because they represent formalized agreements with clear terms, signatures, and documented obligations. For collection agencies utilizing accounts receivable automation, this extended timeframe allows for strategic, phased collection approaches that can incorporate multiple contact methods and negotiation strategies before the statute expires.

Oral Agreements and Open Accounts: Three-Year Limitation

Debts based on oral agreements verbal promises without written documentation and open accounts such as credit cards without written contracts fall under a three-year statute of limitations in Arkansas. This shorter timeframe reflects the reduced evidentiary strength of verbal agreements and the need for more rapid collection action.

Open accounts, particularly retail credit arrangements and utility services, typically operate under this three-year window. For agencies managing high-volume consumer debt portfolios, this compressed timeline necessitates efficient, automated collection workflows. Implementing omnichannel support systems can dramatically improve contact rates and resolution speeds within these tighter statutory boundaries.

Promissory Notes and Court Judgments

Promissory notes formal written promises to pay specific amounts at defined times also carry a five-year statute of limitations in Arkansas. However, once a creditor obtains a court judgment against a debtor, that judgment remains enforceable for ten years and can be renewed for additional ten-year periods, significantly extending the collection window.

This distinction highlights the strategic value of pursuing legal judgment before the initial statute expires. For collection operations, timely litigation decisions can transform time-limited debts into long-term recoverable assets.

Calculating the Statute of Limitations Start Date

Determining when the arkansas statute of limitations on debt collection begins is often more complex than simply identifying the debt type. The 'trigger date' typically corresponds to one of several key events:

- Date of last payment: In most cases, the statute begins when the debtor makes their final payment on the account

- Date of default: When the debtor first fails to meet contractual payment obligations

- Date of charge-off: When the original creditor writes off the debt as uncollectible

- Date of last activity: Any account activity that acknowledges the debt may restart the clock

Research from national statute of limitations benchmarks by state shows that Arkansas's 3-6 year timeframes align with national averages, though some states impose shorter or longer periods. This benchmark data helps collection managers assess compliance risks when operating across multiple jurisdictions.

For agencies employing automated data extraction systems, accurately capturing and monitoring these trigger dates becomes mission-critical. AI-powered platforms can automatically flag accounts approaching statutory deadlines, enabling strategic prioritization of legal action or settlement negotiations.

Time-Barred Debt: Collection Restrictions and Compliance

Once the statute of limitations expires, debt becomes 'time-barred,' creating significant compliance obligations for collection agencies. While collectors may still contact debtors about time-barred debts, they face strict regulatory constraints under both Arkansas law and federal regulations like the Fair Debt Collection Practices Act (FDCPA).

Prohibited Practices with Time-Barred Debt

Collection agencies cannot:

- Threaten or initiate legal action on time-barred debt

- Misrepresent the legal status or collectibility of expired debts

- Fail to disclose that the debt is time-barred when requested

- Use deceptive tactics to restart the statute of limitations

The Consumer Financial Protection Bureau has issued specific guidance requiring collectors to clearly disclose when debts are time-barred, particularly if partial payments or acknowledgments could revive the statute. For organizations managing complex portfolios, implementing compliance-focused AI systems ensures all communications adhere to these evolving regulatory standards.

Revival of the Statute of Limitations

In Arkansas, certain debtor actions can potentially restart or 'revive' the statute of limitations:

- Written acknowledgment of the debt: A signed statement recognizing the obligation

- Partial payment: Making any payment toward the debt balance

- Written promise to pay: Committing to a payment plan or settlement

Collection agencies must carefully document these revival events while ensuring they don't employ coercive or deceptive tactics to obtain them. Modern post-call analysis tools can automatically review collection conversations for compliance with revival disclosure requirements.

Strategic Implications for Arkansas Collection Agencies

Understanding the arkansas statute of limitations on debt collection directly impacts portfolio management, recovery strategies, and operational efficiency. Collection agencies must balance aggressive recovery efforts with compliance obligations, all while maximizing return on investment.

Portfolio Segmentation and Prioritization

Effective collection operations segment accounts based on:

- Time remaining before statute expiration: Accounts approaching deadlines receive priority

- Debt type and limitation period: Three-year debts require faster action than five-year obligations

- Likelihood of revival events: Debtors with payment history may restart the clock

- Cost-benefit analysis: Legal action costs versus potential recovery amounts

AI-powered platforms enable dynamic portfolio segmentation that continuously re-prioritizes accounts based on statute proximity, debtor engagement patterns, and predicted recovery likelihood. This intelligent workflow management dramatically improves recovery rates while reducing compliance risks.

Early-Stage Collection Emphasis

Given the compressed timeframes particularly for three-year oral agreements and open accounts successful Arkansas collection operations emphasize early-stage recovery. Implementing automated batch calling systems allows agencies to contact thousands of recent delinquencies daily, maximizing engagement opportunities during the optimal collection window.

Early-stage collections benefit from higher debtor cooperation, fresher contact information, and less likelihood of disputes. By deploying AI voice agents capable of personalized, empathetic conversations, agencies can resolve accounts before they age into more challenging, statute-threatened territory.

Legal Action Timing Decisions

For accounts approaching statutory deadlines without resolution, collection managers face critical decisions about litigation. Factors influencing these decisions include:

- Debt amount versus legal costs

- Debtor's ability to pay and asset availability

- Likelihood of judgment collection

- Relationship preservation considerations

Agencies serving multiple industries from healthcare debt collection to financial services must tailor litigation strategies to industry-specific debtor profiles and account characteristics.

Leveraging AI and Automation for Statute Compliance

Modern debt collection technology addresses the complex challenge of managing the arkansas statute of limitations on debt collection through intelligent automation, predictive analytics, and compliance monitoring.

Automated Statute Tracking and Alerts

AI-powered collection platforms automatically:

- Calculate statute expiration dates for each account based on debt type and trigger events

- Generate alerts when accounts approach critical deadlines

- Flag time-barred debts to prevent prohibited collection activities

- Track revival events that restart limitation periods

These automated safeguards eliminate human error in statute calculations and ensure collection teams focus efforts on legally viable accounts. For agencies managing tens of thousands of accounts across multiple debt types, this automation becomes indispensable.

Compliance Scripting and Quality Assurance

AI voice agents and conversational AI systems can be programmed with state-specific compliance requirements, ensuring every debtor interaction adheres to Arkansas statute of limitations disclosure obligations. These systems automatically:

- Disclose time-barred status when legally required

- Avoid threatening or suggesting legal action on expired debts

- Document debtor statements that might revive statutes

- Provide consistent, compliant messaging across all channels

Post-interaction quality assurance powered by natural language processing reviews 100% of collection conversations for compliance violations, dramatically reducing regulatory risk compared to traditional sampling methods.

Predictive Analytics for Recovery Optimization

Advanced AI platforms analyze historical collection data to predict which accounts are most likely to resolve before statute expiration, enabling data-driven resource allocation. Machine learning models consider:

- Debtor engagement patterns and contact responsiveness

- Payment history and partial payment likelihood

- Time remaining before statute expiration

- Optimal contact timing and channel preferences

This predictive approach transforms statute limitations from a compliance burden into a strategic advantage, focusing human collector expertise on high-value, time-sensitive accounts while automating routine, early-stage collections.

Industry-Specific Statute Considerations in Arkansas

Different industries face unique challenges with the arkansas statute of limitations on debt collection based on typical debt types, account lifecycles, and debtor demographics.

Healthcare and Medical Debt

Medical debts in Arkansas typically fall under the five-year written contract statute when patients sign treatment agreements, or three-year limitations for services without formal contracts. Healthcare providers and collection agencies must navigate additional federal protections, including HIPAA privacy requirements that complicate debtor verification and communication.

Specialized healthcare collection solutions integrate compliance with both statute limitations and medical privacy regulations, ensuring patient data protection while maximizing recovery within legal timeframes.

Auto Finance and Transportation

Auto loans and transportation industry debts universally involve written contracts with five-year statutes. However, repossession rights and deficiency balances create additional complexity. After vehicle repossession and resale, deficiency balances retain the original contract's statute start date, not the repossession date.

Collection agencies specializing in auto finance recovery must track multiple dates original default, repossession, resale, and deficiency calculation to accurately determine statute status.

Retail and Consumer Goods

Retail credit accounts, store cards, and retail industry receivables predominantly operate as open accounts under three-year limitations. The compressed timeframe demands rapid collection action and sophisticated debtor skip-tracing to maintain contact.

High-volume retail portfolios benefit enormously from end-to-end collection automation that processes thousands of small-balance accounts efficiently within tight statutory windows.

Best Practices for Arkansas Debt Collectors

Collection agencies operating in Arkansas should implement these best practices to maximize recovery while maintaining strict statute of limitations compliance:

- Comprehensive data management: Maintain detailed records of debt origin dates, payment histories, and all debtor communications that might affect statute calculations

- Regular compliance training: Educate collection staff on Arkansas-specific statute requirements and prohibited practices with time-barred debt

- Technology integration: Deploy AI-powered systems that automatically track statutes and prevent non-compliant collection activities

- Early intervention emphasis: Prioritize fresh accounts to maximize resolution opportunities before statute pressures intensify

- Clear documentation protocols: Document all revival events payments, acknowledgments, promises that restart limitation periods

- Legal consultation procedures: Establish clear escalation protocols for accounts approaching statute deadlines requiring litigation decisions

- Transparent debtor communication: Proactively disclose time-barred status when appropriate, building trust and encouraging voluntary payment

These practices, combined with advanced collection technology, create sustainable, compliant operations that maximize recovery rates across account lifecycles.

Frequently Asked Questions

Does making a partial payment restart the statute of limitations in Arkansas?

Yes, making any payment toward a debt in Arkansas can restart the statute of limitations clock, giving creditors a new timeframe to pursue legal collection. Debtors should understand this implication before making payments on old debts, and collectors must ensure they don't employ deceptive tactics to obtain revival payments.

Can collectors still contact me about a debt after the statute of limitations expires?

Yes, collectors may still contact debtors about time-barred debts. However, they cannot threaten or file lawsuits, and they must disclose the time-barred status if asked. Debt doesn't disappear when the statute expires only the legal right to sue for collection.

How does the statute of limitations relate to credit reporting timeframes?

The statute of limitations and credit reporting periods are separate. In Arkansas, while the statute may expire after 3-5 years, negative items can remain on credit reports for seven years from the original delinquency date under federal Fair Credit Reporting Act guidelines. A time-barred debt may still impact credit scores even when no longer legally collectible through courts.

How do I know if my debt is classified as written or oral contract?

If you signed any agreement physical or electronic outlining payment terms, interest rates, and obligations, the debt likely qualifies as a written contract with a five-year statute. If the agreement was verbal or involves standard services without signed terms, it typically falls under the three-year oral/open account category. When uncertain, consult the original creditor or legal counsel.

What should I do if a collector threatens to sue on a time-barred debt?

Threatening legal action on time-barred debt violates both Arkansas law and federal FDCPA regulations. Document the threat, request written validation of the debt including the last payment date, and consider filing complaints with the Arkansas Attorney General's office and the Consumer Financial Protection Bureau. Consult an attorney specializing in consumer rights if a lawsuit is actually filed on an expired debt you can raise the statute of limitations as an affirmative defense.

Conclusion

The arkansas statute of limitations on debt collection establishes critical legal boundaries that profoundly impact collection strategy, operational efficiency, and regulatory compliance. With five-year limitations for written contracts and three-year windows for oral agreements and open accounts, Arkansas collectors must implement sophisticated tracking systems and prioritization frameworks to maximize recovery within these timeframes. Modern AI-powered collection platforms transform statute compliance from a regulatory burden into a strategic advantage through automated tracking, predictive analytics, and intelligent workflow management. By combining deep regulatory knowledge with advanced technology, collection agencies can achieve superior recovery rates while maintaining strict compliance with Arkansas statute requirements and federal consumer protection laws.

Ready to Transform Your Collections Process?

See how CollectDebt.ai can help you automate debt collection, reduce costs, and improve compliance.